Using Municipal Bonds to finance broadband networks

Learn about the Digital Divide and Public-Private Partnerships (P3s) and how they tackle historic public infrastructure delays and cost overruns.

In the telecommunications industry (specifically, the provision of broadband service), broadband incumbents have focused their new construction, expansion and investments in large, populous cities that offer high profits and high returns on investment. Consequently, many rural and low-income urban communities have been left behind regarding access to affordable high speed broadband services, and modern information, communications and technology infrastructure. This dynamic has had a severely negative impact on society and economic growth and contributed to the large and ever growing gap between those who have access to the internet, technology, and digital literacy training and those who do not. This Digital Divide affects people of all ages in all sectors – children who require the internet to complete homework, workers who need digital skills to keep pace with rapidly advancing technology in business, patients who require access to critical healthcare and telehealth services, community members who desire to use important online government services.

Federal, state, and local governments have afforded communities with access to many vital services and infrastructure, including but not limited to highways, roads, bridges, schools, transit systems, and water, wastewater, gas, and electricity utilities. In considering additional services and infrastructure to provide, municipal governments should explore Public-Private Partnerships (P3s) to build fiber broadband networks in or expand to unserved and underserved communities. Historically, public infrastructure projects have faced delays and cost significant overruns. In P3 projects, cost overruns are not common as P3 models divide responsibilities and risks between the public and private sectors depending on their areas of expertise and operational capacity. For example, the public partner may carry the risk of local and/or state laws changing, while the private partner may cover the costs of construction delays and cost overruns.

Public-Private Partnerships

P3s have numerous operating advantages compared to single operation incumbent-led broadband providers. P3 contracts do not include an equity component in the capital structure that would require high rates of return. Thus, private or outside investments can be guided by elements other than profit, such as local economic growth and quality of life. P3s also have access to tax-exempt financing and lower interest rates than large telecommunications corporations. If structured properly, P3s can have access to long term fixed lower interest rates for debt and in smaller increments not typically available for traditional telecommunication providers. Moreover, municipalities and cooperatives may already manage utility systems that could support cross-utilization of resources in the construction and maintenance of a fiber broadband network, such as make ready and pole attachment costs and rights of way.

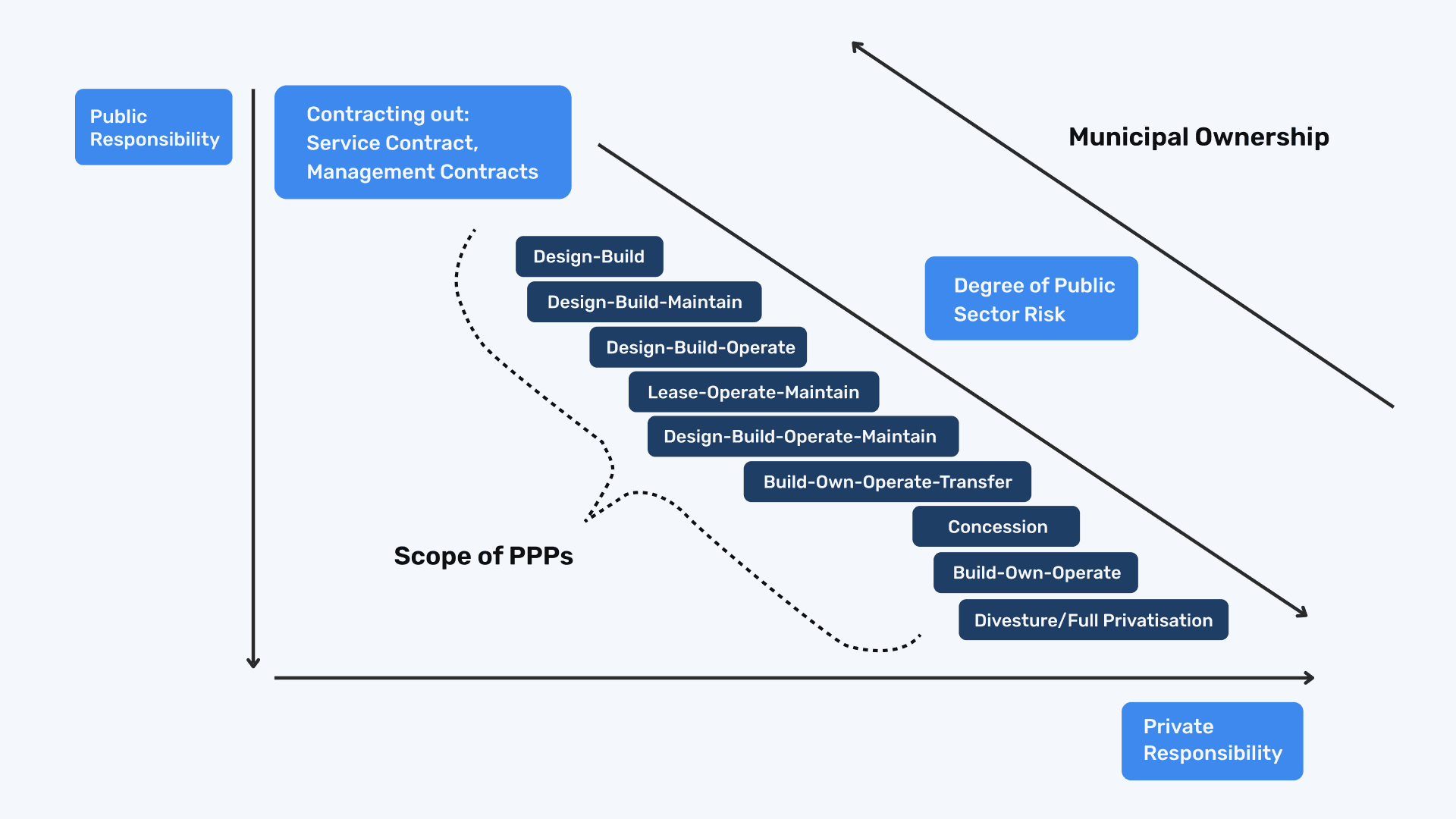

There are various types of P3s contracts, all with different levels of risk transfer, ownership, control, financial efficiency, and public policy support. The following P3s range from more public responsibility to more private responsibility.

- Design-Build: A private partner designs and builds an asset for a public partner.

- Design-Build-Maintain: A private partner designs, builds, and maintains an asset for a public partner.

- Design-Build-Lease-Operate-Maintain: A private partner creates an asset based on a public partner’s specifications and leases it back to the public partner. This is common for P3 prison projects.

- Design-Build-Operate-Maintain: A private partner designs, builds, operates, and maintains an asset for a public partner.

- Build-Own-Operate-Transfer: A private partner builds and owns an asset during the contract period with the aim of recovering construction expenses. When the contract ends, the asset is returned to the public partner. This structure is often used for hospital and school contracts.

- Concession: A private partner has the long-term right to build and operate an asset while the public partner may retain ownership of the asset. The private partner pays the public partner for the concession rights and the public partner may also pay the concessionaire to help projects be commercially viable and reduce the risk the private partner must shoulder. Concession periods typically range from 5 to 50 years.

- Build-Own-Operate: A private partner builds and owns an asset. This model is often used for power or water treatment plants.

Tax-Exempt Bonds

Tax-exempt financing commonly referred to as municipal bonds provides lower interest rates than financing programs from commercial banks. Money can be used to buy, build, or renovate new infrastructure or facilities, refinance higher interest loans or variable rate loans, and purchase major equipment or assets.

There are several types of municipal bonds. General obligation bonds are backed by the taxing power of the issuing municipality. The municipality will pay back interest and principal to all investors through normal taxes or specific bond issues that are approved by voters. Revenue bonds are paid back through funds generated by the project itself. For example, revenue bonds can be sold to fund the construction of a toll bridge. Bond investors are paid back through the tolls generated by the completed bridge. Sometimes a state or local government will create a special bond authority to oversee revenue bond-funded projects like toll roads and bridges, airports, and low-income housing. Industrial revenue bonds are a type of private activity bond which is issued by municipalities on behalf of private organizations (either for-profit or non-profit) to finance the acquisition, construction, rehabilitation, and equipping of manufacturing and processing facilities. The projects subject to financing must benefit the community. For example, broadband projects that will be constructed under the Infrastructure Investment and Jobs Act programs are explicitly eligible for industrial development bonds.

To access the Capital Markets at attractive low interest rates, a borrower must have a solid credit history, and provide a financial model and forecast projections to prove its ability to pay back investors in the future. These elements are typically based on several factors such as a Debt Service Coverage Ratio. The higher the risk, the higher the rate. Lower the risk, the lower the rate. The public market rates (especially tax-exempt) are for the most part much cheaper than private equity and Corporate access to capital allowing public agencies to stretch out fixed terms and provide more leverage to projects.

Is your organization looking to build out a fiber network? Are you interested in learning more about P3s and tax-exempt financing? Please join the broadband.money community today!

Have a suggestion?

We’d love any feedback. Submit here

Related guides & resources

Enroll for free today

It's free. Find out if you qualify for Broadband.money assistance.